Profit and Loss Important Formulas – Aptitude Questions and Answers

Cost Price:

The price, at which an article is purchased, is called its cost price, abbreviated as C.P.

Selling Price:

The price, at which an article is sold, is called its selling prices, abbreviated as S.P.

Profit or Gain:

If S.P. is greater than C.P., the seller is said to have a profit or gain.

Loss:

If S.P. is less than C.P., the seller is said to have incurred a loss.

IMPORTANT FORMULAE:

1. Gain = (S.P.) – (C.P.)

2. Loss = (C.P.) – (S.P.)

3. Loss or gain is always reckoned on C.P.

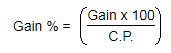

4. Gain Percentage: (Gain %)

5. Loss Percentage: (Loss %)

![]()

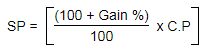

6. Selling Price: (S.P.)

7. Selling Price: (S.P.)

![]()

8. Cost Price: (C.P.)

![]()

9. Cost Price: (C.P.)

![]()

10. If an article is sold at a gain of say 25%, then S.P. = 125% of C.P.

11. If an article is sold at a loss of say, 15% then S.P. = 85% of C.P.

12. When a person sells two similar items, one at a gain of say x%, and the other at a loss of x%, then the seller always incurs a loss given by:

13. If a trader professes to sell his goods at cost price, but uses false weights, then

![]()

Leave a Reply